POS Integration

Turn Every Register Into a Wallet Terminal

The Problem

In-store loyalty is broken. Points programs live in a separate system from payments. Customers forget to scan. Store associates forget to ask. The data sits in a silo that never talks to your e-commerce stack. And you're paying full interchange on every swipe regardless.

Accrue POS fixes this by turning your existing registers into wallet terminals. No hardware swap. No rip-and-replace. Every transaction — regardless of how the customer pays — flows into a single wallet ecosystem where customers earn real money, not points.

Two Ways Into the Wallet

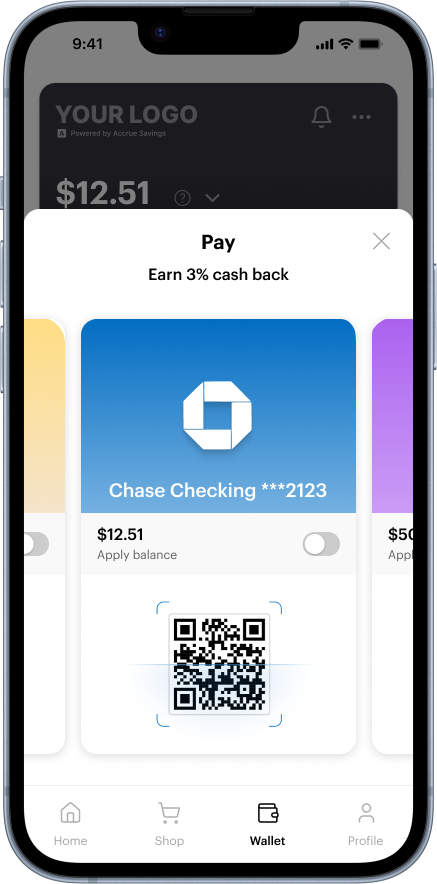

QR Code / Loyalty ID

The customer opens your app at checkout. The cashier scans a QR code — or enters the customer's phone number. Funds are pulled directly from the wallet over ACH. No card network involved. No terminal required. The payment settles via Accrue's Payments API with reduced processing fees.

This is the cleanest path: wallet balance in, payment out, rewards earned, zero swipe.

External Purchase Recognition

The customer pays however they want — their own Visa, cash, Apple Pay, doesn't matter. They give their phone number at checkout. Your POS feed sends the transaction to Accrue. Accrue matches it to their wallet by phone number and generates rewards on spend they were going to make anyway.

This is the unlock. You don't need customers to change how they pay to start building the relationship. They swipe their card, give their phone number, and earn cashback into their Accrue wallet. Over time, the wallet balance grows. They start scanning the QR code instead. Adoption happens organically — not because you forced it, but because the math is better.

Split Tender

A single transaction can combine wallet + credit card + cash. Each tender line is tracked independently. Rewards apply to the eligible portions. Refunds claw back proportionally.

This matters because real in-store transactions are messy. A customer pays $80 with their wallet and $40 on a Visa. The POS sends both tender lines. Accrue matches the wallet portion via card webhook, creates an ExternalPurchase for the Visa portion, and generates the correct reward on each. One transaction, two payment methods, zero manual reconciliation.

Store Channels

Every physical location is a channel. Each channel carries:

- Name, full address, and your POS system's store ID (

externalChannelId) - Custom metadata for anything else you need to track

- Independent performance analytics — filter revenue, transactions, and wallet adoption by location

For chains, bulk import hundreds of locations via CSV or Excel in a single call. Channels appear in settlement reports, analytics, and backoffice automatically.

Integration Paths

You don't need to rebuild your POS. You need to connect it.

| Path | Best For | What Happens |

|---|---|---|

| Batch Feed | Large retailers with existing data pipelines | Transaction + tender files ingested on a schedule. Accrue's adapter layer transforms, matches to wallets, and processes rewards automatically. |

| Real-Time API | Modern POS with webhook support | Your POS calls POST /api/v1/external-transactions on each sale, void, refund, or exchange — with full split-tender detail. |

| Hybrid | Retailers in transition | VDC (tap-to-pay) transactions arrive in real-time via card network webhooks. Non-VDC transactions arrive via batch feed. Both feed the same wallet. |

The real-time API accepts:

- Transaction type — Purchase, Void, Refund, or Exchange

- Source — Your POS transaction ID and timestamp

- Customer — Phone number, email, or loyalty ID for wallet matching

- Channel — Which store location processed the transaction

- Payments — Full split-tender breakdown per line (amount, method, last 4 digits)

Settlement

Different payment modes settle differently. You don't need to think about it — Accrue routes each one correctly.

- Tap to Pay (VDC) — Settles via Accrue's standard settlement. Net or gross. Standard or same-day ACH.

- QR / ACH wallet payments — Settles via Pay by Wallet settlement. Daily batched ACH to your merchant account.

- External purchases — No money moves through Accrue. Only rewards and analytics are generated. Your existing processor settles these the same way it always has.

For full details, see our Settlements Guide.

Why This Isn't Another Loyalty Integration

Traditional POS loyalty bolts a points ledger onto checkout and hopes customers remember to scan. It's a parallel system — separate from payments, separate from e-commerce, separate from the customer's actual financial behavior.

Accrue POS is different in a fundamental way:

- The wallet holds real money. FDIC-insured balances, not points with an expiration date and a confusing conversion rate. Customers fund it, earn into it, and spend from it.

- Every payment method counts. Customers don't need to switch to a proprietary card. They pay however they want and still earn rewards. The wallet grows in the background.

- Online and in-store are the same system. The wallet a customer uses at your register is the same one they use on your website. One balance, one reward history, one relationship.

- Adoption is organic. External purchase recognition means day-one value with zero behavior change. Over time, the wallet balance accumulates and customers start paying with it — because it's free money sitting there. You don't push adoption. You let the economics pull.

Accrue POS turns every transaction at every register into a wallet interaction — regardless of how the customer pays.

Want to see Accrue POS in action?

Contact us at info@byaccrue.com for a demo